Home / Blog / 2017 Maximum HSA Contribution for Individuals Adjusts Upward

2017 Maximum HSA Contribution for Individuals Adjusts Upward

Inflation-based increase to 2017 Maximum HSA

Inflation-based increase to 2017 Maximum HSA

Good News! The IRS has announced an inflation-based adjustment for the 2017 maximum HSA contribution for individual accounts.

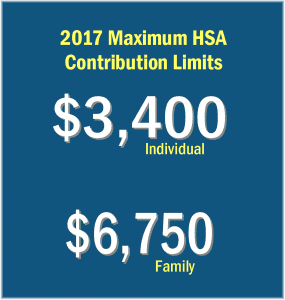

The $50 increase brings the individual maximum tax-deductible contribution limit to $3,400. The maximum HSA contribution for families remains at $6,750 for the new year. Read on for more information on this money-saving plan that benefits both employers and employees.

High Deductible Health Plan and HSA with Section 125 Plan

Gene C Ennis – Bradenton, FL

An HSA is comprised of two parts. The first part is a qualifying high-deductible health plan (HDHP) insurance policy that covers regular medical and hospital bills. The second part of the HSA allows you to make tax-free contributions to an investment account, retirement account, or HSA bank account from which you can withdraw money tax-free for medical care. The HDHP coupled with a Health Savings Account has increased in popularity as employers search for cost-effective ways to provide tax-free health benefits.

For HSA participants fortunate enough to have an employer with a Section 125 Plan modified to allow HSA deductions, tax-free means the participant avoids federal income tax and FICA taxes, which include Medicare and Social Security. This method saves the employee 22.65% to about 40% depending on their tax bracket. The employer also saves matching Social Security (FICA), as well as federal unemployment taxes (FUTA) and generally state unemployment taxes. This extra savings is lost to the employer and the employee if the HSA savings contribution isdeducted from the employee’s gross income on IRS Form 1040.

Here is a short video that gives an excellent explanation of a High Deductible Health Plan coupled with a Health Savings Account (HSA). Employers may further improve tax savings by adding the Section 125 Plan with the HSA savings module. The video was produced a couple of years ago, so the information given reflects contribution limits in effect at the time, but otherwise the information is still current since nothing else about the plans has changed.

Since 1997, Core Documents has been providing free plan design consulting, as well as cost effective, IRS-compliant plan documents to thousands of satisfied agents and employer groups nationwide. An important fact often missed by CPAs, Accountants, Payroll Companies, employers, insurance carriers and agents is how to pre-tax the HSA savings portion going into the investment or HSA bank account. This HSA savings piece can be pre-taxed through an employer’s Section 125 Premium Only Plan. However, the standard Section 125 plan document should be modified or amended to allow the employee to pretax their HSA savings portion through convenient employee payroll deductions. The HSA module is a $30 optional addition to the $99 standard Core Documents Section 125 Plan.

The HSA s a tax-exempt trust or custodial account you set up with a qualified HSA trustee. Clients who wish to provide access to their employees’ HSA can access state of the art, web-based administration services with a debit card optimized for mobile use, from only $9 per month per employee through a new division of Core Documents, CoreAdmin. See /administration.php for more details.

Core Documents provides employers with everything they need to establish an IRS and DOL compliant Section 125 POP Plan for only $99.00 in PDF version emailed to you as soon as your document is completed. For $149, you can receive the Deluxe Binder option that includes the PDF email version ASAP, and a printed plan document in a 3-ring binder shipped via Priority Mail.

You will find information about these fringe benefit plans in the articles below, or call toll free 1-888-755-3373.

Section 125 Premium Only Plan Document – $99 by Core Documents

FSA, HSA, and HRA: What’s the difference?

HSAs, Section 125 POP, and Private Health Insurance Exchanges — Future Trends

Why Every Employer Should Have a Section 129 DCAP FSA Plan